Insurance Handbook

2 Seasons

Season

Health Insurance Playbook

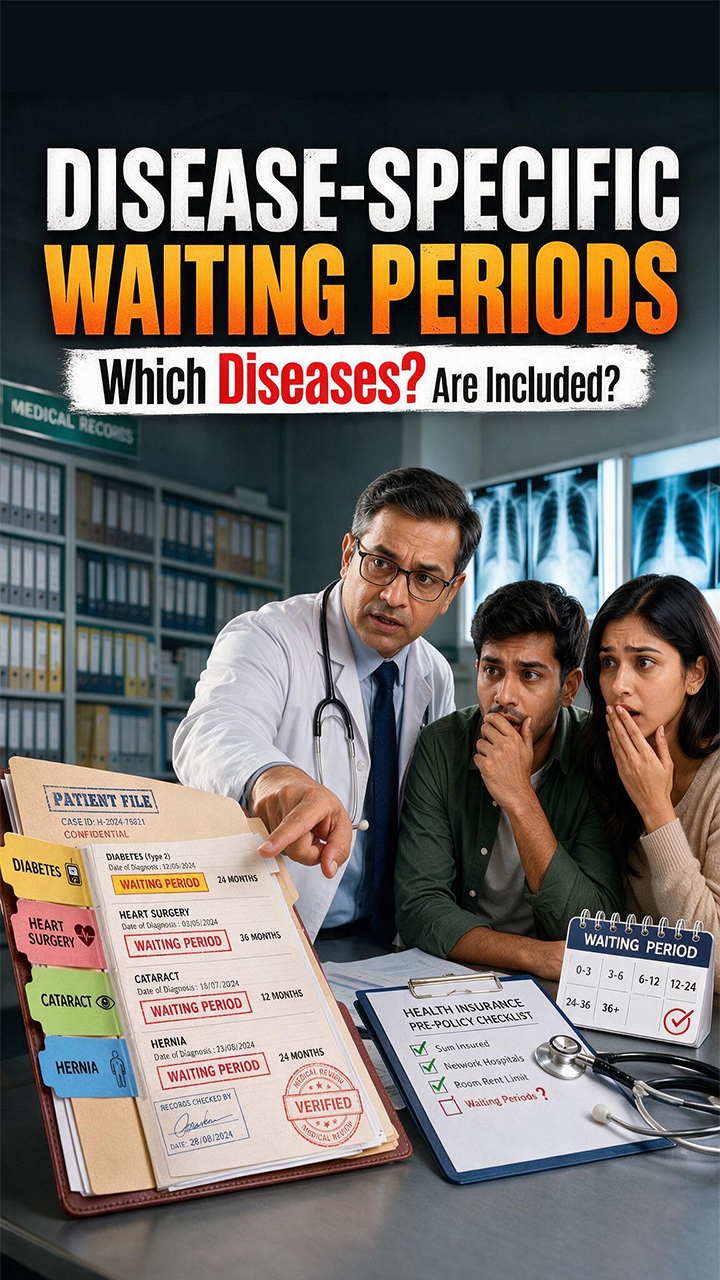

Welcome to the Health Insurance Playbook! This season takes you on an engaging journey through the essential facets of health insurance. We’ll break down the key components of health coverage, helping you find options that align with your lifestyle. Join us as we explore how to maximise your health benefits while uncovering potential tax advantages. Get clarification on important concepts like Mediclaim, cashless claims, reimbursements, etc. to make it easier to navigate the landscape of health insurance. This season will delve into critical areas that health insurance typically covers, along with key exclusions you should be aware of. Understand what deductibles mean for you, know the differences between co-payments and coinsurance, and learn how to switch providers if needed. Lastly, explore vital tips to make informed decisions and debunk five common misconceptions. Get ready to dive into this exciting exploration of health insurance!

Start Watching

Bites

Season

Road Ready with Motor Insurance

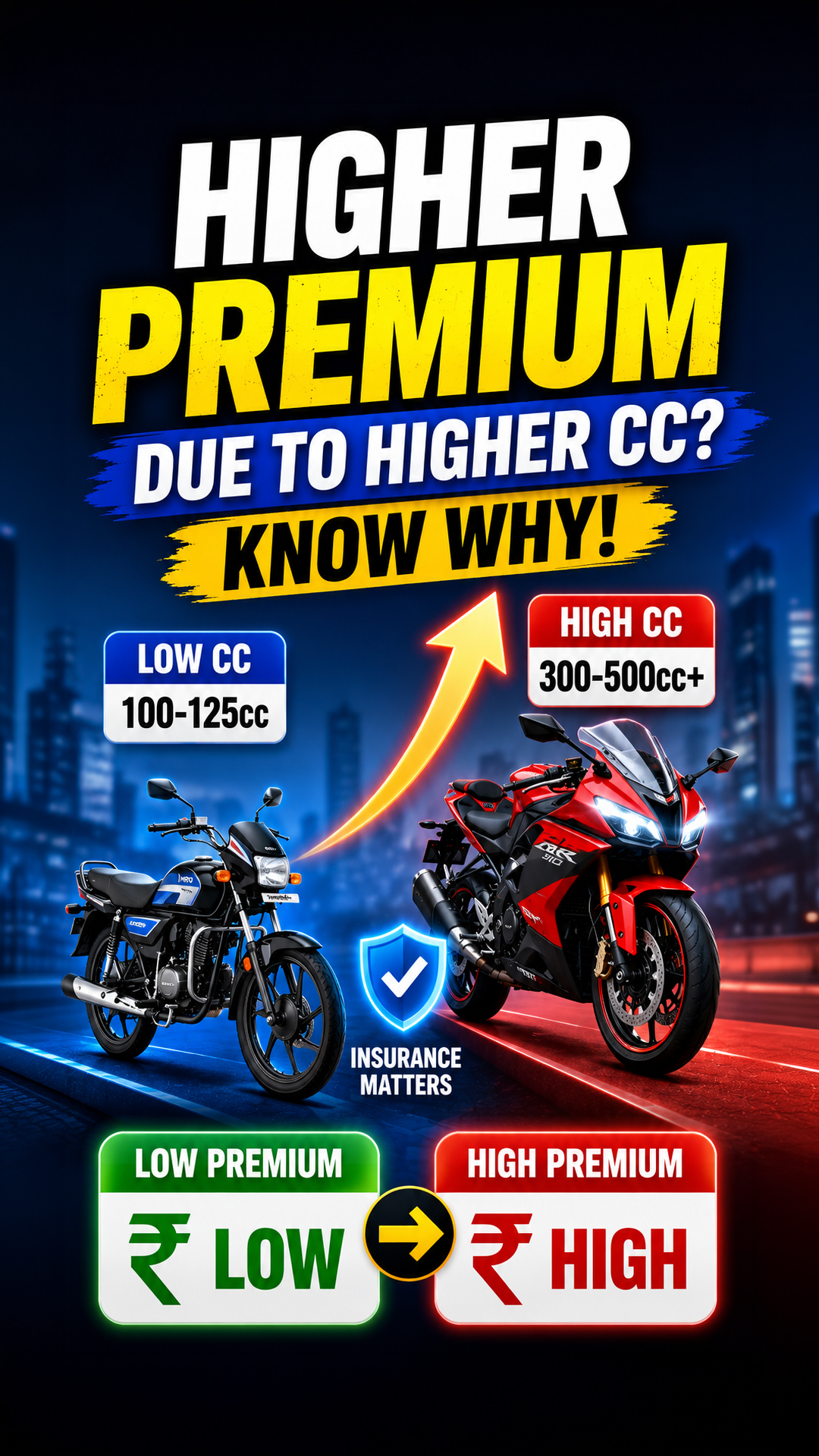

Motor insurance provides financial protection to you and your vehicle. This financial cover is offered against damages and liabilities. To make informed decisions, it's crucial to understand coverage types and policy limits. Different policies offer different coverage options to meet your specific needs. Understanding these choices helps you pick the right coverage. It is also important to understand insurance claims. There are two ways to handle claims: cashless or reimbursement. Each method has its benefits. Knowing what your policy covers helps you assess your protection and find any gaps. Avoid common mistakes when selecting a policy for the best value and protection. Understanding how to file a claim can help you navigate stressful situations smoothly. Similarly, knowing why claims might be denied can help you follow the rules and get your claims approved. In this way, you might be able to utilise, and benefit from your motor insurance.

Start Watching

Bites