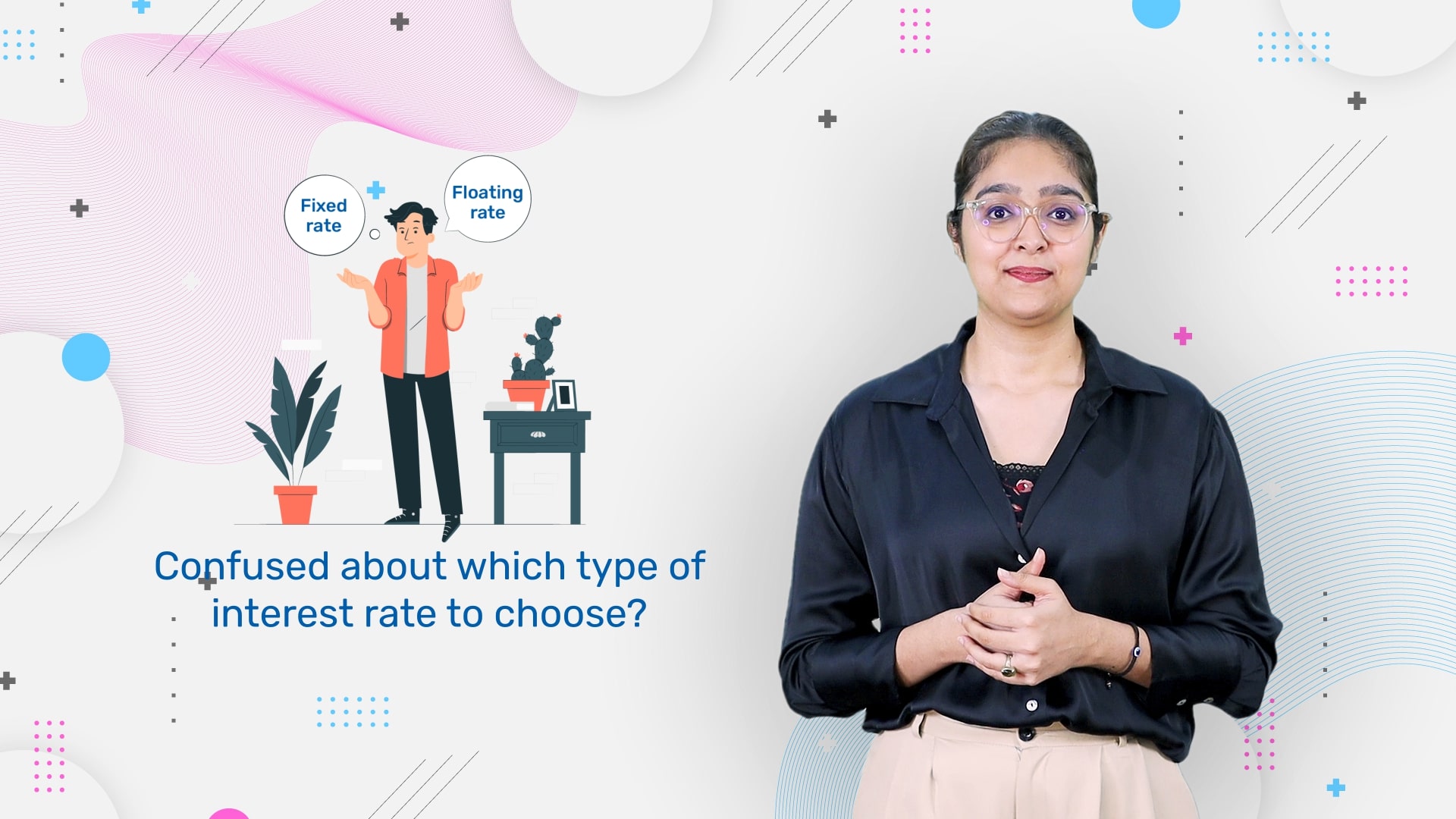

Choosing the right type of interest rate for your home loan could play a crucial role in managing your finances effectively. In this video, we’ll break down the two main types of home loan interest rates in India: fixed and floating.

We’ll start by exploring fixed-rate home loans, which maintain a consistent interest rate throughout the loan tenure. This could offer predictable payments that may simplify budgeting and protect you from market rate hikes. Fixed rates might provide stability if you’re a borrower who prefers certainty in repayment plans.

Next, we’ll discuss floating-rate home loans, which are linked to market benchmarks. This means your interest rate could vary over time. We’ll look at how these loans often start with lower rates, which might make them more affordable initially. Additionally, we’ll cover the flexibility of pre-payment options without penalties, which could help you save on interest if you plan to repay early.

We’ll also consider other factors, like market trends, loan tenure, and risk tolerance, to help you make an informed choice. By understanding these options, you might find it easier to choose a rate that aligns with your financial goals.