Fixed Deposits are popular for their safety and guaranteed returns, yet simple errors could limit their potential. In this video, we’ll look at common mistakes that you could avoid while investing in FDs. We’ll also share a few strategies that might help you make the most of your investment.

One key area we’ll cover is the importance of research. Checking the credibility of banks and financial institutions could be essential, especially since not all FDs are covered by insurance. Only those with banks insured by the Deposit Insurance and Credit Guarantee Corporation (DICGC), a subsidiary of the RBI, are covered. Understanding these details could help you make safer choices.

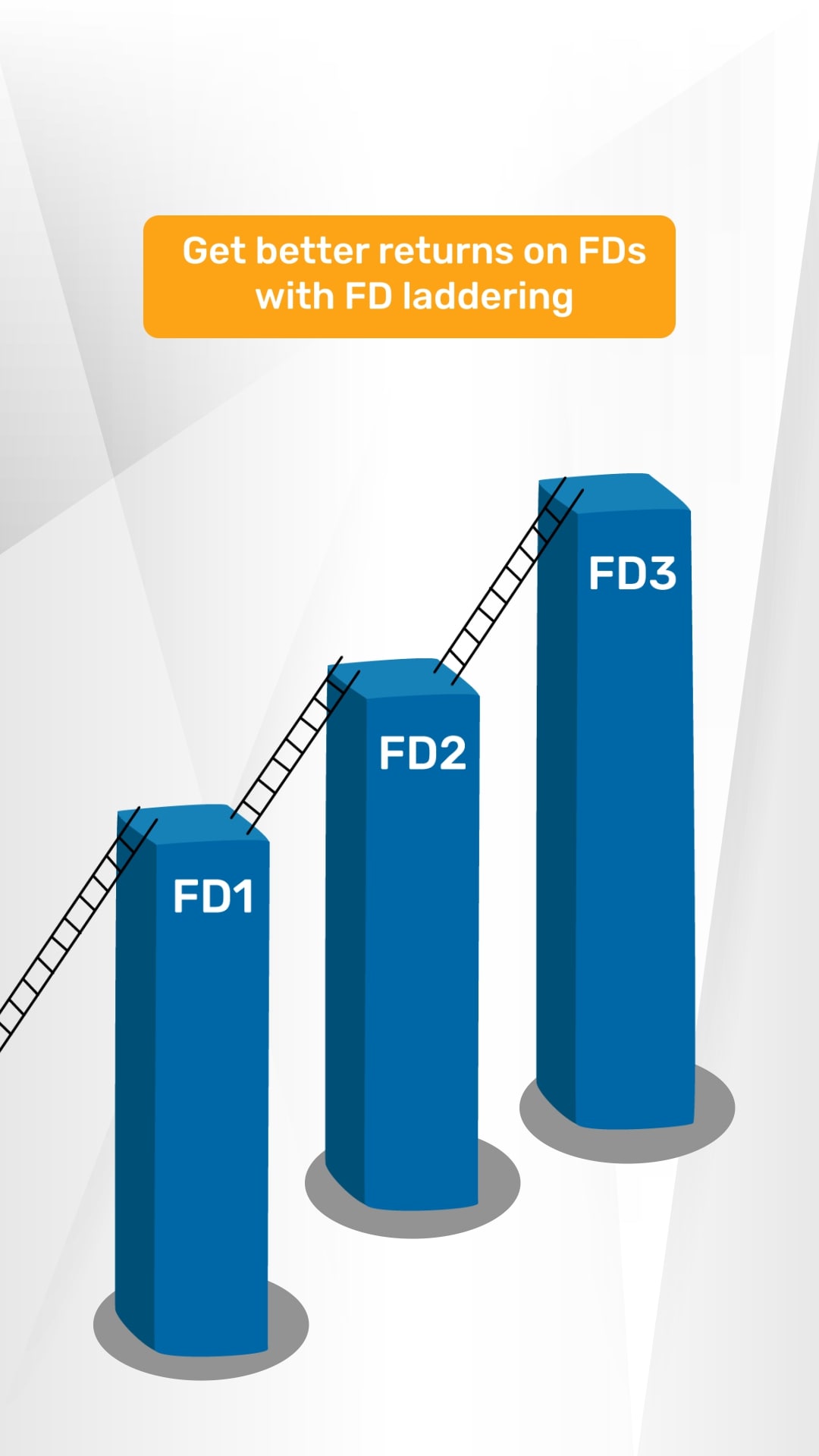

We’ll discuss the impact of interest rates. Even a slight difference could significantly boost your returns over time. Choosing the right tenure to align with your goals could be another important step, as longer terms often yield better rates. Diversifying FDs across various terms and institutions could further enhance your returns and reduce risk.

We’ll also talk about tax implications, planning for premature withdrawal penalties, and the importance of tracking FD renewal dates. By avoiding these common pitfalls, you could manage your FDs effectively and maximise their benefits.