Managing an education loan might seem complicated, but there could be ways to make it simpler and more manageable. In this video, we’ll explore practical strategies to help you manage your education loan with ease.

We’ll uncover how to avoid over-borrowing, calculate your expenses, and choose the right lender based on interest rates, repayment terms, and moratorium periods. We’ll also highlight the benefits of scholarships and financial aid, which could reduce the total loan amount.

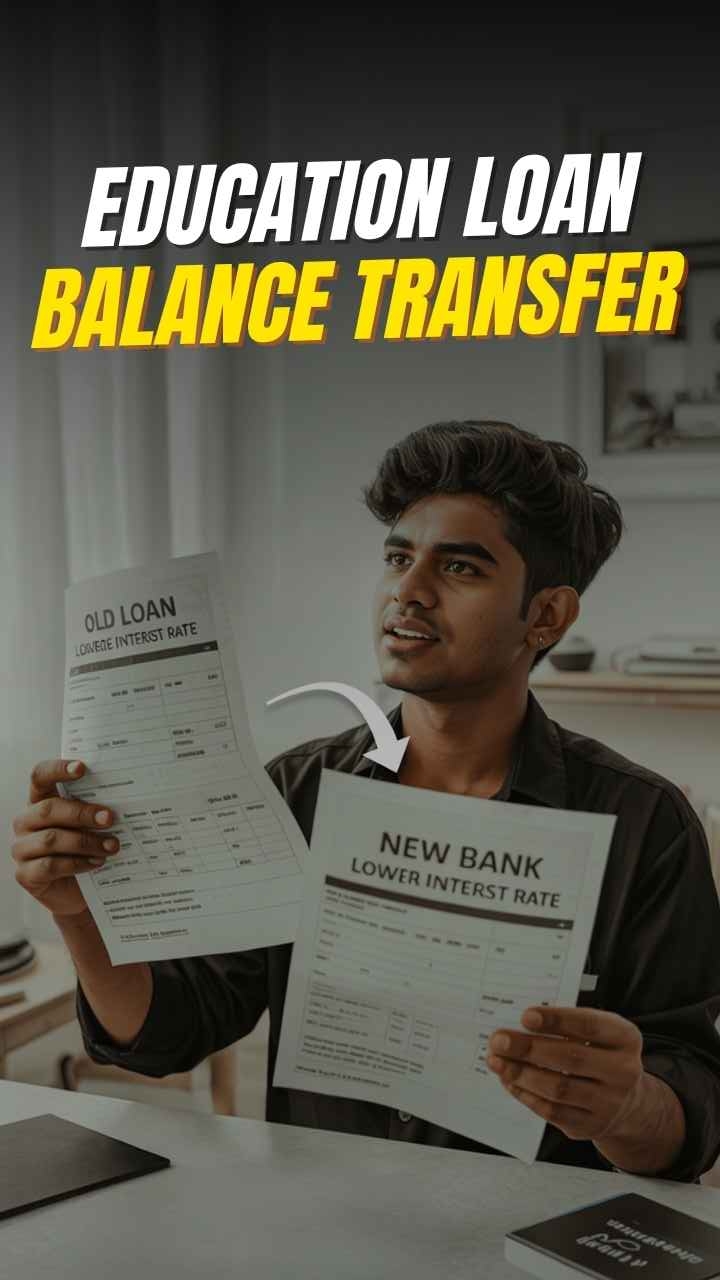

You’ll discover repayment strategies, such as automating EMIs, prepaying the loan when possible, and transferring your loan to a lender offering better rates. We’ll discuss how to manage interest rates, access lender concessions, and benefit from tax deductions under Section 80E of the IT Act.

We’ll also address common repayment challenges, like handling financial hardships or job loss, and show how lenders might support you through repayment restructuring or deferment.

With these strategies, you might be able to manage your education loan more effectively, reduce financial stress, and stay focused on your academic journey.